May 2, 2023 | By Jason Myat, Ruth Aung

May 2, 2023 | By Jason Myat, Ruth Aung

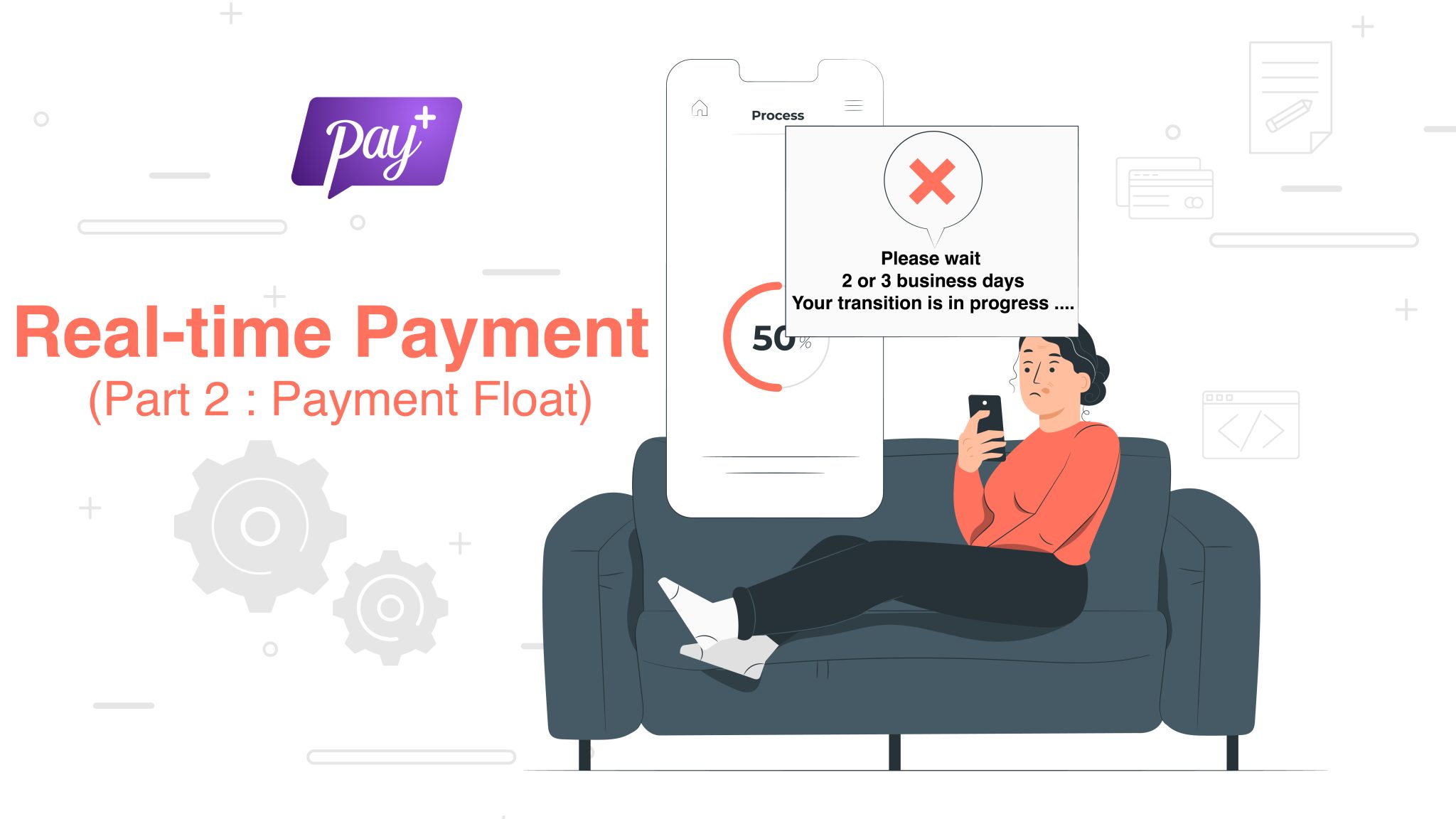

Real-time Payment - Payment Float

Real-time Payment (Payment Float)

Payment systems have evolved throughout the years, moving from cash to checks, credit and debit cards, and finally to mobile payment methods. However, despite these advancements, there are still inefficiencies in payment systems.

Payment systems have evolved throughout the years, moving from cash to checks, credit and debit cards, and finally to mobile payment methods. However, despite these advancements, there are still inefficiencies in payment systems.

Payment Float

Payment Float

Payment delays from a payer to a payee during their transactions lead to economic inefficiency, with substantial implications for both financial institutions and their clients. Non-cash payment methods like paper-based or card-based ones tend to face this most usually. The delay between when a payment is initiated by the payer and when the funds are accessible to the payee is described as the “payment float.” The money is still in progress at this time and cannot yet be used by the payee. The duration may change depending on variables like the chosen payment method and the bandwidth of the banks or other financial institutions involved. Cash flow and financial planning for both the payer and payee may well be affected by the payment float. In order to avoid cash flow issues and assure that payments are paid and received on time, it is essential to understand the payment float and consider it when making decisions while managing finances. On the consumer side, a delay in a pay check that a company issues to an employee may limit that person’s ability to spend money in the short term, thus increasing expenses through the use of short-term financing products. Although if each late payment may have a minimal effect, taken collectively, they might cause a significant financial impact.

Payment delays from a payer to a payee during their transactions lead to economic inefficiency, with substantial implications for both financial institutions and their clients. Non-cash payment methods like paper-based or card-based ones tend to face this most usually. The delay between when a payment is initiated by the payer and when the funds are accessible to the payee is described as the “payment float.” The money is still in progress at this time and cannot yet be used by the payee. The duration may change depending on variables like the chosen payment method and the bandwidth of the banks or other financial institutions involved. Cash flow and financial planning for both the payer and payee may well be affected by the payment float. In order to avoid cash flow issues and assure that payments are paid and received on time, it is essential to understand the payment float and consider it when making decisions while managing finances. On the consumer side, a delay in a pay check that a company issues to an employee may limit that person’s ability to spend money in the short term, thus increasing expenses through the use of short-term financing products. Although if each late payment may have a minimal effect, taken collectively, they might cause a significant financial impact.

Payment Float Problems

Payment Float Problems

As mentioned above about the payment float, the problems the float has created have solutions after the introduction of real-time payments to the users and businesses in some countries. If money is locked up at the respective financial institution of either the payer or the payee, cash accessibility may be limited or even impossible. The overall delay may lead to financial inefficiencies and other potential risks for both individuals and corporations. For most individuals, this might not pose a significant threat, but for business purposes, it creates a series of issues which can prevent the businesses from operating overall.

This can affect cash contingency severely as in the payment float causing a gap in cash flow that can be difficult to manage, particularly if a significant amount needs to be paid. Businesses that go with a steady income stream will find it difficult to operate and have cash contingency in store for emergency financial cases. Every business has a cash contingency, a fund, that a business creates as a support network to cover unforeseen or unplanned expenses or events. Without sufficient funds in the contingency, businesses will be facing financial problems that will have a major impact on business functions. So, to prevent this and to make sure about having sufficient funds in hand, some businesses have to lend money from other financial institutes outside of theirs leading to additional costs in the system.

This can affect cash contingency severely as in the payment float causing a gap in cash flow that can be difficult to manage, particularly if a significant amount needs to be paid. Businesses that go with a steady income stream will find it difficult to operate and have cash contingency in store for emergency financial cases. Every business has a cash contingency, a fund, that a business creates as a support network to cover unforeseen or unplanned expenses or events. Without sufficient funds in the contingency, businesses will be facing financial problems that will have a major impact on business functions. So, to prevent this and to make sure about having sufficient funds in hand, some businesses have to lend money from other financial institutes outside of theirs leading to additional costs in the system.

Additional cost, another risk from payment float which could go beyond the problems of cash contingency as above is also another consequence of payment float. Additional costs include interest rate, late payment fees, administrative expenses, opportunity cost and reputation damage. Using credit to pay expenditures during the payment float can lead to interest and late payment fees while administration expenses will increase to monitor the payments to avoid payment float. The potential revenues or progress that are lost during the payment float might lead to opportunity cost. Additionally, it can also undermine the capacity of a company to handle financial responsibilities if payments are often late or disputes occur as a result of payment float.

Additional cost, another risk from payment float which could go beyond the problems of cash contingency as above is also another consequence of payment float. Additional costs include interest rate, late payment fees, administrative expenses, opportunity cost and reputation damage. Using credit to pay expenditures during the payment float can lead to interest and late payment fees while administration expenses will increase to monitor the payments to avoid payment float. The potential revenues or progress that are lost during the payment float might lead to opportunity cost. Additionally, it can also undermine the capacity of a company to handle financial responsibilities if payments are often late or disputes occur as a result of payment float.

As payment float can lead to economic inefficiency where both financial institutions and their clients face substantial implications, this can become a major threat to any transaction made. Therefore, businesses and individuals should consider implementing real-time payments to reduce payment inefficiency. To learn how real-time payment can counter these payment inefficiencies, stay tuned for the article part 3.